Posted by Leonard Steinberg on June 5th, 2013

{kind=link}

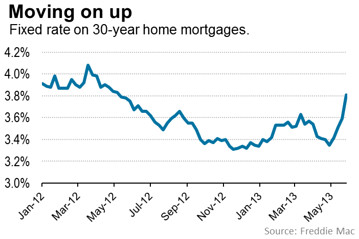

The Wall Street Journal asks the question whether rising interest rates could stop the improving housing markets in the USA. Interest rates have climbed past 4% in the past month. The truth of the housing market is that in the hardest hit areas, prices fell so low as to be below the future expected cash flows from their rental values. So Wall Street stepped in with bag-loads of very cheap cash(yes, that is why it is mostly cash sales because no one else has that kind of cash), to take advantage of these distressed bargains. This could explain why this housing recovery has been so narrow and bifurcated.

If interest rates rise, the return on investment models will become more challenging to hit. It doesn’t matter if they have no “mortgage”, the rate of return is benchmarked versus something and 10-year Treasuries is probably one benchmark used. The buyer needing a mortgage will have tougher hurdles to hit to be eligible under Fannie and Freddie “conforming loan” rules, especially since so many middle class workers are experiencing declining real wages. All of this barely applies to real estate sales in Manhattan, but this could certainly alter the mood of the US markets in general.